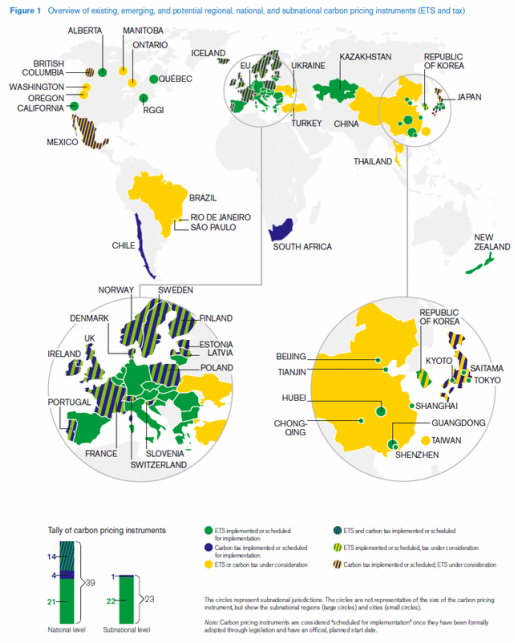

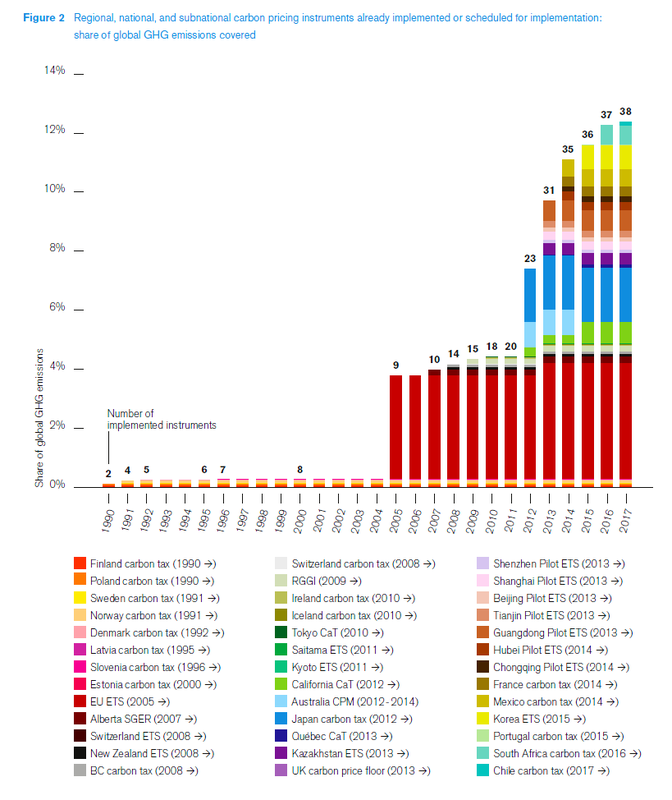

. With the countdown on to the Paris climate change conference, there is clear evidence of growing momentum to put a price on carbon. The growth of carbon pricing around the world has been substantial. Since January 2012, the number of carbon pricing instruments already implemented or scheduled for implementation has almost doubled, jumping from 20 to 38. Moreover, the share of emissions covered by carbon pricing has increased threefold over the last decade.

Currently, about 40 national jurisdictions and over

20 cities, states, and regions—representing almost a

quarter of global greenhouse gas (GHG) emissions—are

putting a price on carbon (Figure 1). Together,carbon

pricing instruments cover about half of the emissions in

these jurisdictions, which translates to about 7 gigatons of

carbon dioxide equivalent (GtCO2e) or about 12 percent

of global emissions (see Figure 2).

To date, China and the United States are the two

countries with the largest volume of emissions covered

by carbon pricing instruments. In China carbon pricing

instruments cover 1 GtCO2e, while in the United

States they cover 0.5 GtCO2e. China has announced its

intention to move to a national emissions trading system

(ETS). It currently has seven pilot ETSs, which combined

form the largest national carbon pricing initiative in

the world in terms of volume. The European Union

Emissions Trading System (EU ETS), which covers

2 GtCO2e of emissions, remains the single largest

international carbon pricing instrument.

So far this year, the Republic of Korea launched an ETS, and California and Québec’s cap-and-trade programs expanded their GHG emissions coverage from about 35 to 85 percent by including transport fuel.

Also, Ontario announced its intention to implement

an ETS linked to California and Québec’s programs. A

major structural reform in the EU ETS was approved

for implementation starting in 2019, and a proposal

to revise the EU ETS after 2020 has been put forward.

These changes should make the EU ETS more resilient

to sudden changes in macroeconomic conditions and

help ensure that the EU ETS enables cost-effective

emission reductions in the decade to come.

The advances in 2015 follow on the heels of 2014

milestones such as the implementation of two new

subnational ETSs in Hubei and Chongqing (both

Chinese jurisdictions), the implementation of carbon

taxes in France and Mexico, and the adoption of new

tax legislation in Chile. The year has also seen more

companies using an internal price on carbon.

Carbon pricing is increasingly being used internally

by firms as a tool to analyze business and investment

strategy. Some of these carbon prices are substantially

higher than current price levels in mandatory carbon

pricing instruments. Internal carbon pricing is part of

a risk management strategy to evaluate the current or

potential impact of a mandated carbon price on business

operations. It is also used as a means to identify and

value cost savings and revenue opportunities in low carbon investments.

In a world of fragmented carbon pricing instruments,

the potential impact of carbon pricing on the international

competitiveness of some domestic industrial sectors has

been a concern. The risk of carbon leakage is real as long

as carbon price signals are strong and the stringency of

climate policies differs significantly across jurisdictions.

However, the report finds, based on available

research, that carbon leakage—the phenomenon of

companies moving their production and/or redirecting

their investments to other jurisdictions where emissions

costs are lower, thereby increasing emissions there—has

not materialized on a significant scale. This risk tends to

only affect a limited number of exposed sectors, namely

those that are both emissions- and trade intensive. This

risk can be effectively managed through policy design

components, such as free allocations, exemptions,

rebates and border adjustment measures, as well as

specific complementary measures, for example, financial

assistance.

The risk of carbon leakage declines as more countries

take concrete actions to prevent climate change.

International cooperation through carbon pricing

instruments and climate finance can help redress the

existing asymmetry in carbon pricing signals, reduce

concerns about their impact on competitiveness, and

eliminate the need for protection of firms. Under these

circumstances, carbon prices can be used to enhance

the performance of economies—specifically benefiting

innovative, low-carbon firms, and promoting the

technical upgrade or exit of the least efficient firms in

emissions-intensive industries. This would improve the

overall efficiency of the economy.

In addition to reducing the risk of carbon leakage,

cooperation between countries can significantly reduce

the overall cost of achieving a 2°C climate stabilization

goal compared to domestic actions alone, as countries

have more flexibility in choosing who undertakes

emission reductions, and who pays for them. Moreover,

such cooperation could drive low-carbon growth in

lower-income countries, some of which might lack the

resources to modernize their economies, create jobs in

low-carbon sectors, or reduce poverty in a sustainable

manner. Through international cooperation, the global

costs associated with a given emission reduction target

can be lowered or a larger mitigation target can be

achieved at a given cost, and development gaps can be

narrowed.

According to estimates from economic models,

financial transfers through cooperation could reach

up to US$100–400 billion annually by 2030, possibly

increasing to over $2 trillion dollars by 2050. The size

of the transfers will be beyond the level of public sector

spending, and will need to be channeled through a blend

of instruments. These include carbon pricing instruments

such as ETSs, carbon taxes, offsets and a combination

thereof and linkages between them, as well as innovative

hybrid instruments, such as variations of results-based

climate finance. Climate finance and carbon pricing

instruments will be essential in leveraging these financial

transfers and enabling cooperation to mitigate climate

change.

Currently, about 40 national jurisdictions and over

20 cities, states, and regions—representing almost a

quarter of global greenhouse gas (GHG) emissions—are

putting a price on carbon (Figure 1). Together,carbon

pricing instruments cover about half of the emissions in

these jurisdictions, which translates to about 7 gigatons of

carbon dioxide equivalent (GtCO2e) or about 12 percent

of global emissions (see Figure 2).

To date, China and the United States are the two

countries with the largest volume of emissions covered

by carbon pricing instruments. In China carbon pricing

instruments cover 1 GtCO2e, while in the United

States they cover 0.5 GtCO2e. China has announced its

intention to move to a national emissions trading system

(ETS). It currently has seven pilot ETSs, which combined

form the largest national carbon pricing initiative in

the world in terms of volume. The European Union

Emissions Trading System (EU ETS), which covers

2 GtCO2e of emissions, remains the single largest

international carbon pricing instrument.

So far this year, the Republic of Korea launched an ETS, and California and Québec’s cap-and-trade programs expanded their GHG emissions coverage from about 35 to 85 percent by including transport fuel.

Also, Ontario announced its intention to implement

an ETS linked to California and Québec’s programs. A

major structural reform in the EU ETS was approved

for implementation starting in 2019, and a proposal

to revise the EU ETS after 2020 has been put forward.

These changes should make the EU ETS more resilient

to sudden changes in macroeconomic conditions and

help ensure that the EU ETS enables cost-effective

emission reductions in the decade to come.

The advances in 2015 follow on the heels of 2014

milestones such as the implementation of two new

subnational ETSs in Hubei and Chongqing (both

Chinese jurisdictions), the implementation of carbon

taxes in France and Mexico, and the adoption of new

tax legislation in Chile. The year has also seen more

companies using an internal price on carbon.

Carbon pricing is increasingly being used internally

by firms as a tool to analyze business and investment

strategy. Some of these carbon prices are substantially

higher than current price levels in mandatory carbon

pricing instruments. Internal carbon pricing is part of

a risk management strategy to evaluate the current or

potential impact of a mandated carbon price on business

operations. It is also used as a means to identify and

value cost savings and revenue opportunities in low carbon investments.

In a world of fragmented carbon pricing instruments,

the potential impact of carbon pricing on the international

competitiveness of some domestic industrial sectors has

been a concern. The risk of carbon leakage is real as long

as carbon price signals are strong and the stringency of

climate policies differs significantly across jurisdictions.

However, the report finds, based on available

research, that carbon leakage—the phenomenon of

companies moving their production and/or redirecting

their investments to other jurisdictions where emissions

costs are lower, thereby increasing emissions there—has

not materialized on a significant scale. This risk tends to

only affect a limited number of exposed sectors, namely

those that are both emissions- and trade intensive. This

risk can be effectively managed through policy design

components, such as free allocations, exemptions,

rebates and border adjustment measures, as well as

specific complementary measures, for example, financial

assistance.

The risk of carbon leakage declines as more countries

take concrete actions to prevent climate change.

International cooperation through carbon pricing

instruments and climate finance can help redress the

existing asymmetry in carbon pricing signals, reduce

concerns about their impact on competitiveness, and

eliminate the need for protection of firms. Under these

circumstances, carbon prices can be used to enhance

the performance of economies—specifically benefiting

innovative, low-carbon firms, and promoting the

technical upgrade or exit of the least efficient firms in

emissions-intensive industries. This would improve the

overall efficiency of the economy.

In addition to reducing the risk of carbon leakage,

cooperation between countries can significantly reduce

the overall cost of achieving a 2°C climate stabilization

goal compared to domestic actions alone, as countries

have more flexibility in choosing who undertakes

emission reductions, and who pays for them. Moreover,

such cooperation could drive low-carbon growth in

lower-income countries, some of which might lack the

resources to modernize their economies, create jobs in

low-carbon sectors, or reduce poverty in a sustainable

manner. Through international cooperation, the global

costs associated with a given emission reduction target

can be lowered or a larger mitigation target can be

achieved at a given cost, and development gaps can be

narrowed.

According to estimates from economic models,

financial transfers through cooperation could reach

up to US$100–400 billion annually by 2030, possibly

increasing to over $2 trillion dollars by 2050. The size

of the transfers will be beyond the level of public sector

spending, and will need to be channeled through a blend

of instruments. These include carbon pricing instruments

such as ETSs, carbon taxes, offsets and a combination

thereof and linkages between them, as well as innovative

hybrid instruments, such as variations of results-based

climate finance. Climate finance and carbon pricing

instruments will be essential in leveraging these financial

transfers and enabling cooperation to mitigate climate

change.

RSS Feed

RSS Feed